CALLS/WHATSAPP: +254 707 30 30 85 / +254 788 91 44 55 | Avg. Response Time: 10 mins | Client Retention: 95% | Trusted by 100+ Cleints | Claims Updates: Every 48 hrs | Get the Best Rates & Discounts ! T&Cs...

We're here to help you get back on track. Please provide the details of your incident below to start your claims process. Once submitted, we will review your information and reach out shortly to guide you through the next steps.

An insurance policy is a promise of compesation when things go wrong provided you fall within the policy’s terms and conditions.

If you are lucky, you may never have to make a claim against your insurance policy. However, when things go wrong and you are involved in an unexpected accident, sickness, disaster or experience loss that is covered by your insurance policy you can make a claim with your insurer.

What is a claim?

The claims process is similar across different insurance types, though motor insurance may involve vehicle assessments for repairs or replacements, while Health and WIBA insurance have longer criteria.

Insured should contact their agent or insurance company promptly after an event, especially for theft or serious accidents. Reviewing your policy can help confirm if you have a valid claim and if the event is not excluded. Having all necessary information and docuents makes the claim process straightforward.

Filing an insurance claim can feel stressful, but following the right steps can simplify the process. Whether you face a minor accident, a major collision, or theft, this guide helps you navigate the claim process confidently and efficiently.

Steps To Follow Based on Incident;

The steps you follow after an incident depend on three critical factors:

Understanding these factors will allow you to determine the best approach to file your claim.

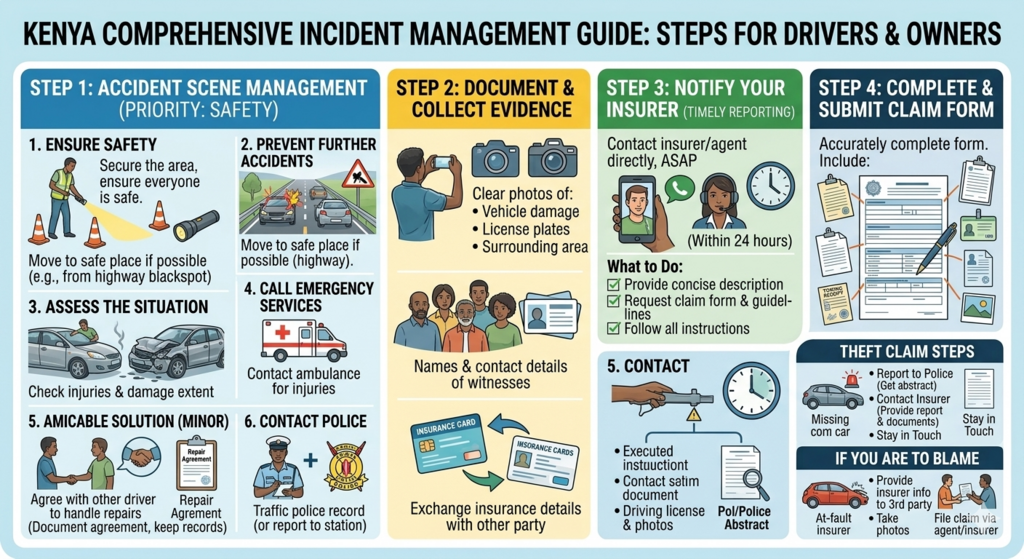

Steps To Follow When You Get an Accident;

Managing the accident scene is the first priority. Proper handling ensures safety and lays the groundwork for your claim.

Start by securing the area and ensuring everyone is safe:

2. Prevent futher accidents;

Check for immediate dangers, especially on busy highways or blackspots and move to a safe place if you are in a place where further accidents can occur

3. Access the situation

Check for injuries, damage extent [Minor or major] and determine if it’s safe to remain at the scene

4. Call for emmergency services

Contact an ambulance if injuries are present. Timely medical attention can save lives and prevent complications.

5.Amicable solution (minor accidents)

If the accident is minor, you can agree with the other driver to handle repairs without involving insurance or authorities. Document the agreement and keep repair cost records as evidence.

6. Contact the police

Traffic police usually visit accident scenes to record statements. If they don’t, call them or report to the nearest station to obtain a police abstrat.

Whether the accident is minor or major, collect evidence accurately to support your claim:

Once the immediate situation is under control, contact your insurer directly or through your agent as soon as possible. Most insurance companies require notification within 24 hours.

What to Do When Notifying Your Insurer

Accurately completing the claim form is critical to a successful claim. Include all necessary details and evidence collected at the scene.

What to Include in the Claim Form

How To File a Theft Claim

If your vehicle is stolen, follow these simple steps:

What To Do if You are to Blame for The Accident ?

If you cause damage to someone else’s vehicle or property, follow these steps:

After you submit your motor insurance claim, the insurer follows these steps:

The insurance company assigns an assessor to inspect your vehicle, review damage, and prepare a report. A recommended garage will also provide a repair estimate, which the assessor compares to finalize the repair costs.

2. Investigations ( if needed)

Depending on the accident’s nature, the insurer may assign an investigator to confirm the claim’s validity and check for compliance with policy terms.

3. Claim Decision

The insurer reviews all findings and issues a decision. If approved, you’ll receive an authority letter with repair costs, timelines, and conditions. If rejected, they will provide reasons for the denial.

What Happens If an Insurance Claim is Approved?

If the insurance company accepts your claim, the insurer provides an authority letter indicating repair costs, timelines, and conditions. With the authority letter, the repair of your vehicle can begin.

Compesation options

If you prefer a specific garage, the insurer can release funds for you to manage the repairs. You should keep receipts for any expenses and submit them for reimbursement.

What To Expect When a Vehicle Is Declared a Write-Off

If damage exceeds 60% of the car’s value (varies by insurer), the vehicle is written off.

Payment Timeline

Insurers must pay within 90 days per the Insurance Regulatory Authority (IRA). Top-tier insurers may pay faster, while lower-tier companies might take longer.

A third-party claim occurs when you are sued in a court of law for causing loss or injury to another party (the third party). Follow the steps below.

Making a medical claim generally follows two paths: Direct Settlement (Cashless) at a network provider or Reimbursement for out-of-pocket expenses

Direct Settlement (Cashless Claim)

This is the most common method when visiting a hospital within your insurer's approved network.

Reimbursement Claim

Used if the insured visit a non-network provider or pay for services upfront (e.g., pharmacy bills) or last expense benefits.

Follow these steps

compensation is made to insured bank account or Mpesa.

Timeline: Claims must typically be submitted as soon as possible but not latter then 45( consult for specific policy) days of treatment; late submissions may be time-barred.

A medical claim may be declined for several administrative, clinical, or policy-related reasons.

Common Reasons for Claim Denial

How to Respond to a Declines

If a claim is declined, the insurer is generally required to provide a written explanation identifying the specific reason. You can:

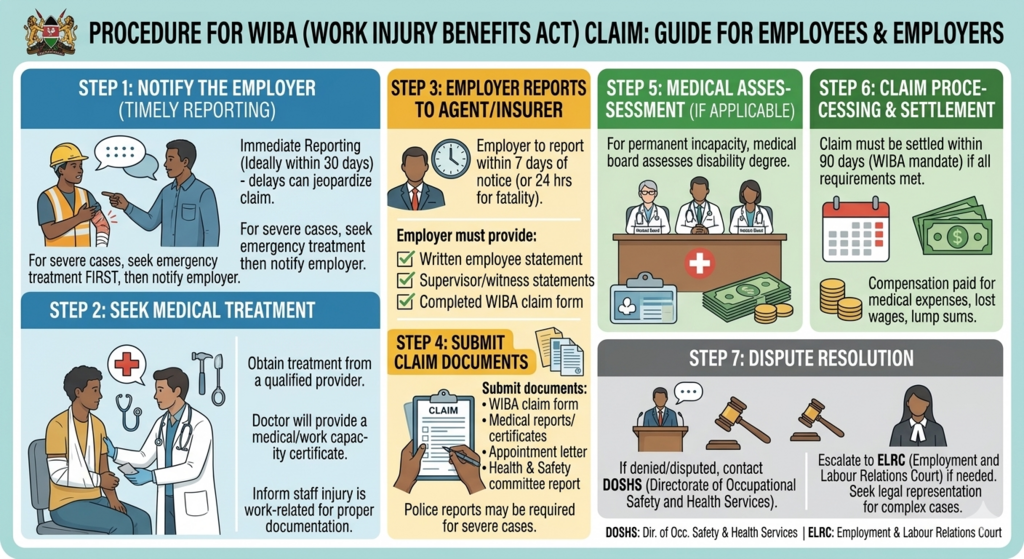

PROCEDURE FOR WIBA CLAIM

Step 1: Notify the Employer

Step 2: Seek Medical Treatment

Step 3: Employer Reports to the Agent or directly to insurance.

Step 4: Submit Claim Documents

Step 5: Medical Assessment (if applicable)

Step 6: Claim Processing and Settlement

Step 7: Dispute Resolution

Common Challenges in Work Injury Claims

Delayed Reporting: Failing to report an injury promptly can result in claim denial. Employees should notify their employer immediately after an incident.

Incomplete Documentation: Missing medical reports or witness statements can create delays or jeopardize the approval of claims.

Disputes: Employers or insurers may challenge the work-related nature of the injury, potentially necessitating legal intervention.

Employees Responsibilities:

- Maintain thorough records of the incident, including photographs, witness names, and medical receipts.

- Seek legal counsel if a claim is denied or if the offered compensation is unsatisfactory.

- Ensure prompt communication with both the employer and insurer to adhere to deadlines.

Employers Responsibilities:

- Invest in comprehensive Workers’ Compensation Insurance tailored to the specific risks of your industry.

- Provide training for employees on workplace safety to minimize incidents and ensure compliance with OSHA regulations.

- Collaborate closely with your insurer to streamline the claims process and prevent disputes.

Your Excellent Intermediary!

We’ll walk with you through the insurance journey!